Mular — making crypto payments easier to trust

A crypto-to-Naira and stablecoin payment platform for people moving money and businesses settling it, without needing to understand blockchain to trust it.

The problem

Mular set out to serve people and businesses moving value between crypto and Naira: diaspora Nigerians sending money home, merchants wanting Naira settlement, and small businesses holding stablecoins against currency volatility. The alternatives asked those users to understand blockchain, manage wallets, monitor rates, and navigate P2P marketplaces. Too much cognitive load, too much risk, too much friction.

Design philosophy

- Hide the technology. No wallet addresses, transaction IDs or blockchain confirmations unless something goes wrong. Show outcomes, not processes.

- Design for the outcome. People don’t want to “convert USDT to NGN”. They want “my family in Lagos receives ₦50,000 by tomorrow”.

- Trust through familiarity. Make it feel like a bank transfer, borrowing patterns from the Nigerian mobile banking apps users already trust.

Key design decisions

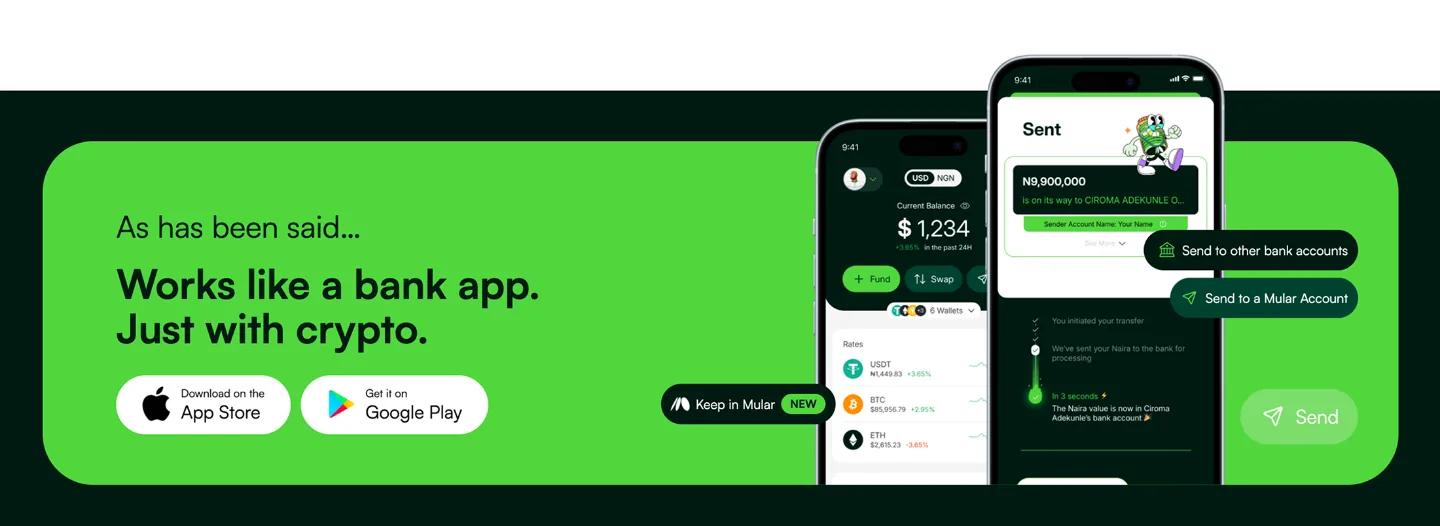

The send flow was designed so a user enters an amount (crypto or Naira — the product handles conversion), sees what the recipient gets before the confirm step, and then follows the transfer through plain-language status instead of hashes, gas, or network-vs-service fees. The screens below show this shipped: a dollar-denominated balance with Fund, Swap and Send actions, live per-asset rates, and a status trail that ends at “the Naira value is now in the recipient’s bank account”.

Design decisions that removed friction

- Wallet management moved to the backend. Users see a Naira balance, not wallet addresses, token balances or blockchain confirmations.

- Fees shown before commitment, not at checkout. The calculator states the full cost upfront so there's nothing left to discover at the confirm step.

Impact

The figures cover live production use of the send, swap and settlement flows described above: individuals converting stablecoins to Naira, and business accounts settling in Naira. They are a snapshot of the platform’s recorded activity, not a controlled measurement of any single screen.